Earned Value Management: Difference between revisions

| Line 136: | Line 136: | ||

</math> | </math> | ||

A ratio equal 1.0 indicates that performance is efficient and on target. A ratio greater than 1.0 indicates excellent, highly efficient performance. A ratio less than 1.0 indicates poor, inefficient performance. <br> | |||

[[File:CPISPI.PNG|400px|right|thumb|Figure <ref name="Frank" />]] | [[File:CPISPI.PNG|400px|right|thumb|Figure <ref name="Frank" />]] | ||

====Example==== | ====Example==== | ||

Revision as of 07:12, 26 September 2015

Earned Value Management (EVM) is a method for measuring a project’s performance. Earned Value Management is a complex task of controlling and adjusting the baseline project schedule during execution, taking into account project scope, timed delivery and total project budget. [1]. The method is useful during execution of a project because it tells us where we are going with schedule and costs, indicating any variance to plan.

Earned Value is based on an integrated management approach that provides one of the best indicator of true cost performance, available with no other project management technique. Earned Value requires that the project’s scope be fully defined, and that a bottom-up baseline plan be put in place to integrate the defined scope with the authorized resources in a specified frame. [2]

Introduction

An important part of successful project management is to have accurate and reliable information and the current performance is the best indicator of future performance. By using trend data, it is therefore possible to forecast cost and schedule overruns early in the project.

Background

The Earned Value Management method was introduced in the 1960s as a financial analysis specialty in United States Government programs, but has since been a significant branch of project management. In the late 1980s and early 1990s, it was no longer used by EVM specialists only. The EVM was emerged as a project management methodology to be understood and used by managers and executives also, and today EVM has become an essential part of project tracking in many projects.

The method can be used to measure the real progress of a project, and combines the measurements of the project management triangle: scope, time and cost. Thereby the EVM method provides early indications of expected project results based on project performance and highlights the possible need for corrective action. These indications become available to management as early as 20 percent into the project [2].

The EVM Method

First of all, to implement the Earned Value method it requires that a Work Breakdown Structure (WBS) must be built by decomposing all the work to done in work packages. These work packages are the smallest groupings of work tasks which are necessary for the level of control needed. Material, labor and other resources are allocated to each work package, and a schedule of all the work packages are set up. [1].

With the EVM method we can measure the expected total project time and cost and calculate the deviation between the current performance and the planned performance. The method uses some basic EVM metrics, which will be introduced.

The Metrics

EVM uses three key parameters to measure project performance [4].:

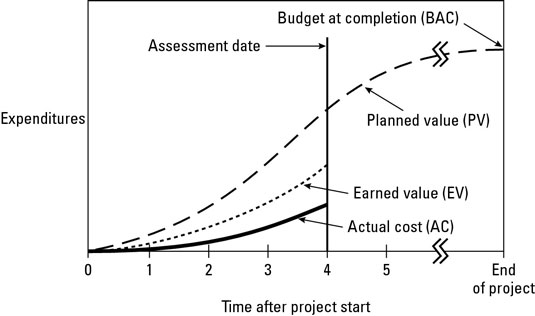

- Planned Value (PV) or Budgeted Cost of Work Scheduled (BCWS)

- This is the time-phased budget baseline. It is the approved budget for accomplishing the activity or work related to the schedule. PV can be viewed as the value to be earned as a function of project work accomplishments up to a given point in time. The total PV is equal to the Budget at Completion (BAC). This is the total budget baseline for the activity or work package. It is the highest value of PV and the last point on the cumulative PV curve. The graph of cumulative PV is often referred to as the S-curve, because it (almost) looks like the letter S.

- Actual Cost (AC) or Actual Cost of Work Performed (ACWP)

- This is the cumulative actual cost spent to a given point in time to accomplish an activity or work (and to earn the related value).

- Earned Value (EV) or Budgeted Cost of Work Performed (BCWP)

- This is the cumulative Earned Value for the work completed up to a point in time. It represents the amount budgeted for performing the work that was accomplished by a given point in time. The EV equals the total budget at completion (BAC) multiplied by the percentage activity (or project) completion (PC) at the particular point in time <math> (=BAC \times PC) </math>

In Figure 2 the three key parameters are shown together with the Budget of Completion (BAC). From this figure it is seen that the Earned Value (EV) is below Budget of Completion (BAC), which means that the project is delayed. Moreover, the figure shows that Actual Cost (AC) is below both BAC and EV. This means that the project is under budget.

There exist four different possible time/cost scenarios, which can be seen on Figure 3.

Scenario 1: The project is late and over budget.

Scenario 2: The project is late but under budget.

Scenario 3: The project is early, but over budget.

Scenario 4: The project is early and under budget.

Example

A project has a total budget at completion (BAC) of $100.000. Then a Work Breakdown Structure (WBS) can be used to break down the different activities. A work package 1.1 has a budget of $20.000 and is 100% complete as of the status date. Thereby, the Earned Value for this work package is:

<math>

\begin{align}

EV = $20.000 \times 1.00 = $20.000

\end{align}

</math>

Work Package 1.2 has a budget of $40.000 and is 50% complete, and the Earned Value is:

<math>

\begin{align}

EV = $40.000 \times 0.5 = $20.000

\end{align}

</math>

The Earned Value for the entire project is:

<math>

\begin{align}

EV = $20.000 + $20.000 = $40.000

\end{align}

</math>

The Planned Value as of the status date is PV = $50.000, but the Actual Cost is AC = $60.000 and the Earned Value is EV = $40.000. This means that the project is over budget and delayed. This example can be seen on Figure 4.

Performance Measurements

By comparing the three key parameters, PV, AC and EV, it is possible to determine the cost performance and schedule performance. The variances are based on cumulative data (also called inception-to-date data and project-to-date data).

Variances

- The Cost Variance (CV) is the difference between the Earned Value (EV) and the Actual Cost (AC), i.e. a measure of budgetary conformance of actual cost of work performed. In other word, CV indicates how much over or under budget the project is.

- <math>

\begin{align} CV = EV - AC \end{align} </math>

- The Schedule Variance (SV) is the difference between the Earned Value (EV) and the Planned Value (PV), i.e. a measure of the conformance of actual progress to the schedule. So in other words, SV indicates how much ahead or behind schedule a project is running.

- <math>

\begin{align} SV = EV - PV \end{align} </math>

Example

If we go back to the example mentioned above, we can calculate the cost variance and the schedule variance.

- <math>

\begin{align} CV = EV - AC = $40.000 - $60.000 = -$20.000 \end{align} </math>

- <math>

\begin{align}

SV = EV - PV = $40.000 - $50.000 = -$10.000

\end{align}

</math>

The CV and SV for this example are shown in Figure 5.

Performance Indices

The performance indices are ratios, which say something about the efficiency.

- The Cost Performance Index (CPI) is the ratio of Earned Value (EV) to the Actual Cost (AC), i.e. a measure of budgetary conformance of Actual Cost of work performed.

- <math>

\begin{align} CPI = {EV\over AC} \end{align} </math>

- The Schedule Performance Index (SPI) is the ratio of Earned Value (EV) to the Planned Value (PV), i.e. a measure of the conformance of actual progress to the schedule. The SPI provides information about schedule performance of the project. It is the efficiency of the time utilized on the project.

- <math>

\begin{align} SPI = {EV\over PV} \end{align} </math>

- The product of the Cost Performance Index (CPI) and the Schedule Performance Index (SPI) is called the cost-schedule index, or the Critical Ratio (CR). This ratio is an indicator of the overall project health, and it informs you of how much you are getting out of each dollar spent on the project.

- <math>

\begin{align} CR = {CPI \times SPI} \end{align} </math>

A ratio equal 1.0 indicates that performance is efficient and on target. A ratio greater than 1.0 indicates excellent, highly efficient performance. A ratio less than 1.0 indicates poor, inefficient performance.

Example

If we need to find the cost performance index (CPI) and the schedule performance index (SPI) for the above project, we can calculate it by:

- <math>

\begin{align} CPI = {EV\over AC} = {$40.000 \over $60.000} = 0.67 \end{align} </math>

- <math>

\begin{align} SPI = {EV\over PV} = {$40.000 \over $50.000} = 0.80 \end{align} </math>

From theses indices we see that both the CPI and SPI are less than 1.0, which indicates that we are a little behind schedule and a lot over budget.

Forecasting

It is said that bad news known at the 20% point in a project’s life cycle gives an opportunity to take corrective actions. [2] Therefore, project managers are primarily concerned with decisions affecting the future, as forecasting and predictions are very important aspects of project management. The EVM is designed to keep an eye of the project performance and to give management an important “early warning” signal to take corrective actions in the future. EVM is especially useful in forecasting the total project cost and time to completion, based on the actual performance up to a given point in the project.

The formula for predicting a project’s final cost, i.e. how much money it will take to complete a given project, is given by the Estimated Cost at Completion (EAC). EACs may differ based on the assumptions made about future performance, and therefore there different variations of EAC exists.

- Variances are typical

- The method is used when the variances at the current stage (or until now) are typical, for example due to some unforeseen conditions which are likely to happen at the beginning of a project, but are not expected to occur in the future.

- <math>

\begin{align} EAC &= AC + (BAC - EV) \\ &= BAC - CV \\ \end{align} </math>

- Past estimating assumptions are not valid

- This method is used when past estimating assumptions are not valid and new estimates are applied to the project. This could for example be if you are behind schedule or over budget.

- <math>

\begin{align} EAC &= AC + {BAC - EV \over CPI \times SPI}\\ &= AC + ETC \\ \end{align} </math>

- Where ETC is the Estimate to Complete.

- Variances will be present in the future

- Here we assume that the future variances and performance will be the same as the past variances and performance, i.e. the CPI will remain the same for the rest of the project.

- <math>

\begin{align} EAC &= AC + {BAC - EV \over CPI} \\ &= {BAC \over CV} \\ \end{align} </math>

EVM vs. Traditional Cost Management

There is a fundamental distinction between using a traditional cost control approach and the Earned Value management. In traditional project cost management the plan-versus-actual cost comparison gives no way to ascertain how much of the physical work that has been accomplished. Such displays merely represent the relationship of what was planned to be spent versus the funds actually spent.[2]

If we take a look at another example and look at the cost performance on top of Figure 4, it indicates great results against the original spending plan, where the planned funds are equal to the actual costs. This is only useful as a reflection of whether a project has stayed within the funds authorized by management, i.e. funding performance. This does not reflect the actual cost performance.[2]

In contrast, Earned Value Management displays three dimensions of data: the Planned Value of the physical work authorized, the Earned Value of the physical work accomplished and the Actual Costs incurred to accomplish the Earned Value. Thus, under an earned value approach, the two critical variances may be ascertained. The schedule variance, SV, shows that the project is experiencing a negative schedule variance of $100.000 from its planned work. This shows that the project management team is clearly behind the planned schedule. When used together with other scheduling techniques, for example The Critical Path Method (CPM), it could provide invaluable into the true schedule status of the project. The other variance, namely the cost variance, CV, we see that the project has a cost overrun of $100.000 for the work performed to date. Experiences has shown that such cost overruns tend to get worse over time, and it is therefore of critical importance to the project. [2]

Limitations

Even though the EVM method is very useful, it has some limitations too. Earned Value as a technique is effective in the management of projects, but has very limited utility in the management of continuous business operations. [2] Therefore it should only be used on projects – preferable on small and simple projects, as large projects has many components which have to be accounted for which can derail in the details. Another crucial aspect is that the EVM method does only consider time and cost, but not the quality. Quality is such an important part of any project, that it necessary to have some kind of quality control. Without that, it means that a project can be on budget and time, but still be a very bad product. Overall, it is also important to remember that the EVM does not tell the whole story, and therefore is the method not attended to be used as a stand-alone tool. [5]

References

- ↑ 1.0 1.1 1.2 Measuring Time: Improving Project Performance Using Earned Value Management (2009), Vanhoucke, M.

(A book about how to improve project performance using Earned Value Management. Provides both case studies and simulation studies, and how to scheduling projects with a software.) Cite error: Invalid<ref>tag; name "Measuring" defined multiple times with different content - ↑ 2.0 2.1 2.2 2.3 2.4 2.5 2.6 2.7 Earned Value Project Management (2005), Fleming, Q. and Koppelman, J.,

(A leading book within Earned Value Project Management. A lot of background for The Earned Value Managament method and how it has envolved through time.) - ↑ http://media.wiley.com/Lux/23/246523.image0.jpg

- ↑ 4.0 4.1 4.2 4.3 Earned Value Project Management Method and Extensions (2003), Anbari, F.

(The paper shows the major aspects of Earned Value Management method and presents a lot of tools graphical. Some extensions on how to use the method even further.) - ↑ How Earned Value Management is Limited (2013), http://www.brighthubpm.com/monitoring-projects/10056-how-earned-value-management-is-limited/

(Short about the limitations on the Earned Value Managment method.)

{kind=link}