Earned Value Analysis

In order to measure performance in terms of cost, time and work progress, the Earned Value Analysis (EVA) is introduced as a suitable method, offering quantitative analysis techniques as well as objective performance indicators [1].Besides giving an overview of the method itself and the steps, which must be followed in order to carry out an EVA, the requirements on both structural and methodological level are presented and the key benefits are outlined. In addition to its’ primary area of application as a tool within project controlling, the extended usability of the method in other key functions of a company is shown. All technical contents are being demonstrated based on illustrative examples.

Terms and definitions

The Earned Value Analysis is defined as a quantitative technique of performance measurement, using estimates of both work progress and related cost to determine the overall efficiency of a respective activity, work package or project[1]. In order to do so, it compares the scope of the project, the schedule of work and the work undertaken in order to determine the status, the likely completion and the out-turn cost of the observed object.

The basic values, which are used in this calculation are the following[2]:

The Planned Cost (PC) are the budgeted cost of the work, which must be completed according to a specified schedule. It is therefore also referred to as the Budgeted Cost of Work Scheduled (BCWS) or as Planned Value (PV) and includes all labour, material, and other cost which is related to specific working steps.

The Actual Cost (AC) describe the cost of the work which has already been accomplished and can also be called the Actual Cost of Work Performed (ACWP)

The Earned Value (EV), also called the Budgeted Cost of Work Performed (BCWP) is an indicator for the value of the work accomplished. It can be determined by calculating the percentage of the total budget which is actually completed at that specific point of time:

| Earned Value (EV) = Total Budget x Work Progress |

These values then serve to calculate additional indicators, which describe how the actual values deviate from the planned values and thus provide important information on how the project is doing.

The Cost Variance (CV) is the algebraic difference between the earned value and the actual cost:

| Cost Variance (CV) = Earned Value (EV) - Actual Cost (AC) |

A positive value indicates a favourable condition. A negative value indicates an unfavourable condition. The cost variance may be expressed as a value for a specific period or as a cumulative value to date.

The Schedule Variance (SV) is a metric for the schedule performance derived from EV metrics and, as the algebraic difference between earned value and planned value, indicates if the progress is on schedule.

| Schedule Variance SV = Earned Value (EV) - Planned Value (PV) |

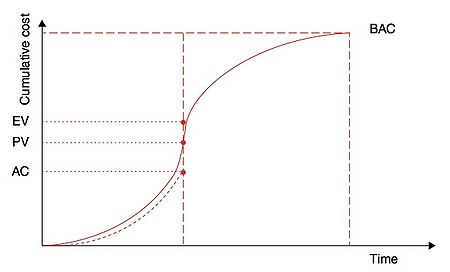

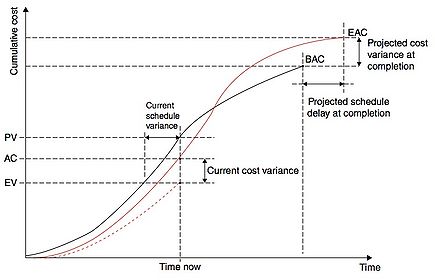

Figure 2 shows a typical curve of the cumulated PV for a project. The exact form of this curve will vary for each project depending on the activities, costs and timing of the construction work. Figure 3 illustrates the relation between PV, AC and EV, Figure 4 additionally shows the cost-and schedule variance:

-

Figure 2 - Planned Value Curve

Figure 2 - Planned Value Curve -

Figure 3 - Planned Value, Actual Cost and Earned Value. In this favorable scenario, the EV exceeds the planned value, and the AC is even below the PV

Figure 3 - Planned Value, Actual Cost and Earned Value. In this favorable scenario, the EV exceeds the planned value, and the AC is even below the PV -

Figure 4: Schedule Variance (SV) and Cost Variance (CV), as well as predicted values at completion

Figure 4: Schedule Variance (SV) and Cost Variance (CV), as well as predicted values at completion

The Budget at Completetion (BAC) describes the total planned budget of a project or work package, and thus the total value which is to be created when completed. When re-estimations or re-scheduling is taking place, the resulting new value is called Estimate at Completion (EAC), which will be specified in detail later on in the chapter Forecasting

The Schedule Performance Index (SPI) is the ratio of the EV divided by the PV ("How are we doing against the plan?"), usually expressed as a percentage.

| Schedule Performance Index (SPI) = Earned Value (EV) / Planned Value (PV) |

The Cost performance Index (CPI) as the ratio between the earned value and the actual cost represents an indicator for the cost effectiveness of the work accomplished.

| Cost Performance Index (SPI) = Earned Value (EV) / Actual Cost (AC) |

Requirements and Process of Preparation

In order to successfully execute an Earned Value Analysis, the following systematic preconditions and requirements must be fulfilled[3]

1) Time-based schedule

The measurement of progress is made on the basis of a work schedule, which must be defined and agreed, including a clear timeline and an estimation of time required per individual activity (s. Figure 5).

2) Work Breakdown Structure

All tasks and their specific scope must be defined separately in the form of a work breakdown structure, which is the basis for performing an EVA. It provides a multi-level structure for analyzing the project at varying degrees of detail. Generally it is a hierarchical structure, in which each lower level represents a split into a single component from the level above. Therefore, it as well serves to control the progress of major working steps through tracking the individual activities it consists of, as for the exact allocation of cost which follows afterwards. It is the responsibility of management authority to ensure, that each individual activity within the WBS is discrete and manageable[4].

3) Cost Assessment

A cost collection system including an appropriate association of cost estimates must be implemented and executed in order to provide exact estimates of the effort of a certain activity (s. Figure 5). Whereas some activities are directly linked to the consumption of materials, usage of machines, purchases of products and services or travels, the most valuable cost commodity is probably time. Tracking the labour time it takes to fulfill a certain work package represents a major task within assessing it’s cost. Therefore, a direct link to the schedule is given at this point, often leading to a re-assessment of the schedule made[4]. The cost can then be cumulated, often generating the traditional S-curve of the project plan. By doing so continuously in the course of the working process, the actual cost, as well as the cost for given time periods, e.g. per week/month can be obtained.

4) Progress measurement

An objective, consistent, quantitative method of assessing progress is required. Whereas certain activities can be measured easily, using e.g. the meters of track layed of a certain road or cubic meters of concrete poured compared to the total, other activities require the definition „earning rules“ to evaluate how much of the work is accomplished[4]. By defining mid-activity milestones and the percentage share of the total, which can be verified easily, this can be achieved, e.g. completion of the preliminary research (10%), the first draft of a drawing (30%), it’s review and the second draft (70%) as well as finalization (90%) and approval by client (100%). These mid-milestones should furthermore be supported by evidence as the issue of documents, minutes of meeting, memos or reports.

5) Responsibility/ authority matrix

A definition of responsibilities and authorities, is key to the success of an EVA. On the one hand, each task within the WBS must clearly be linked to a responsible team member who is in charge of execution and reporting of progress. When it comes to delays or other changes in project parameters, these must be communicated and approved by the respective authorities in order to take suitable countermeasures supported by all stakeholders.

6) Monitoring and review process

In order to identify changes in the course of the project, a monitoring process of all variables must be implemented. The system used must be appropriate to the organization, and furthermore agreed by all participants and parties involved in the project. Within this reviewing process, critical steps and constraints of scope, schedule and cost must be carefully controlled. Any changes in these are to be identified, approved and then recorded through updating the anticipated values against the performance baseline. In this respect, an adequate reporting system should be created to facilitate the information exchange.

Areas of application

Organizational Level - Earned value management System (EVMS)

Fulfilling the requirements for an EVA stated above represent a challenge for organizations, but at the same time, when executed systematically, it can lead to an overall growth of maturity and transparency throughout the entire value chain. Therefore, these measures can be embedded in an Earned value management System (EVMS), using a dedicated process, procedures, tools and templates.

The Electronic Industries Alliance (EIA) has release a standard regarding EVMS which contains a set of 32 Guidelines, defines the requirements that an Earned Value Management System (EVMS) must meet. These guidelines represent a management approach on organizational level, that once incorporated on any type of program, whether research and development, construction, production, etc. provides all levels of management with early visibility into cost and schedule problems. It addresses EVMS in 5 different dimensions:

- Organization

- coordinate all departments involved in the project tasks

- definition of their strategic relationship to product deliverables

- identification of who is responsible (Organization breakdown structure, OBS)

- Planning, Scheduling and Budgeting

- Budgeting and resource allocation system

3) Accounting Considerations

4) EVMS Analysis and EVMS Management Reports

5) Revisions and Data Maintenance

Reference: National Defense Industrial Association, Integrated Program Management Division (2014), EIA-748-EVMS Standard, Revision C Intent Guide, p. 4-51

Project Controlling

As pointed out earlier, the EVA method perfectly serves the purpose of controlling entire projects. Using the Work Breakdown Structure in order to monitor the elements of work at the required level of detail, the Planned Value (PV) can be assessed. This can either be done by simply allocating a proportion of the total PV to each activity, or by predicting the time, materials and other cost factors related to it. Using the agreed project schedule, the cumulated PV over time can then be used in the following calculations to measure performance on the project.

Example:

The creation of a drawing for a design project consists of 6 different activities. Now that the monthly reporting to the management is to be prepared, an assessment of the current progress of the project (at this specific point of time) is made using EVA. The following values have been determined:

| Activity | BAC | Planned Value | Completion (%) | Earned Value | Actual Cost | Schedule Variance | Cost Variance |

|---|---|---|---|---|---|---|---|

| 1 | 80€ | 80€ | 100 | 80€ | 60€ | 0 | +20 |

| 2 | 80€ | 80€ | 100 | 80€ | 100€ | 0 | -20 |

| 3 | 100€ | 100€ | 100 | 100€ | 90€ | 0 | +10 |

| 4 | 100€ | 100€ | 50 | 50€ | 60€ | +50 | -10 |

| 5 | 150€ | 100€ | 50 | 50€ | 70€ | -50 | -20 |

| 6 | 150€ | 0 € | 33 | 50€ | 50€ | +50 | 0 |

| Total | 660 | 460 | 410 | 430 |

As defined earlier, the budget at completion (BAC) defines the value which is to be created by the individual activity when finished whereas the PV is the budgeted value which, according to the plan, is to be accomplished at that specific point of time. In the example activity 5 should be started but not be completed entirely at this point of time, whereas activity 6 hasn't been started at all according to plan. The calculation for activity 5 are exemplarily calculated as follows:

Earned Value: EV(5) = PV x Progress (%) = 150€ x 50% = 75€

Schedule Variance: SV(5) = EV - PV = 50€ - 100€ = -50€

Cost Variance: CV(5) = EV - AC = 50€ - 70€ = -20€

Generally, the analysis reveals that activities 4 and 5 are in fact the ‘problem activities’. Both are behind schedule and over cost. It is also noted from the table that activity 1 was completed under the original budgeted cost but activity 2 was over budget. According to the data collected, Activity 6 is ahead of schedule and on cost.

Schedule Performance Index (SPI) = 410€ / 480€ = 0,89

Cost performance Index (CPI) = 410€ / 430€ = 0,95

The SPI < 1 indicates that the project is clearly delayed significantly, whereas the CPI < 1 reveals an unfavorable situation in terms of cost efficiency.

Kedi and Hongping (2010) furthermore provide guidance for an interpretation for the SPI, including recommended actions (s. Table 1)

| SPI Value Range | Interpretation | Corrective action |

|---|---|---|

| >1,0 | progress is ahead the schedule | - |

| <1,0 | progress is behind the schedule | s.b. |

| 0.9< SPI <1.0 | delay within normal range | adjustment of schedule not required |

| 0.8< SPI <0.9 | slight delay | adjustment of schedule not required, Increase use existing resources, Adding additional resources to be considered |

| 0,7 <SPI <0.8 | considerable delay, causing the risk to not finish the work | adjust schedule, additional resources needed |

| SPI <0.7 | critical delay, high risk for the project | re-schedule, re-estimate planned resources, solve source of delay using additional management reserves |

| SPI >1.3 | significant advance in the progress of the project | check for errors in assessment of workload, re-schedule plan, re-estimate resources |

Table 1: Interpretation of SPI[5]

Forecasting

Link [5]

he Forecast of Project Future Trends and D erences The actual cost and progress of the remaining tasks should be estimated every week, which can determine the pro ess of the project ture trends. 1) Estimated remaining task cost to complete TC) ETC = (the spent cost of ongoing but uncompleted work + expected cost of the ongoing but uncompleted work + budget cost of the not yet started work ) x adjustment coef cient. The estimate of adjustment factor has a certain subjective and it depends on the cost performance index (Cpr), personal problems in weekly report and risks. 2) Estimated cost at completion (EA EAC = ACWP + ETC. EAC is the sum of the actual cost of the task which has been completed and the estimated cost of the remaining tasks, that is the actual cost plus the estimated cost of the remaining tasks which re ecting the current assessment of the estimated total cost. 3) Estimated completion date (ECD) ECD calculation will consider the re ned agenda and some other factors. The revised completion date can be adjusted through the evaluation of the following factors. a) Schedule performance index (SPJ). a) Anticipated sta ng changes. b) Individuals questions and issues listed in the weekly report. b) Risk 4) Estimated cost variance at completion (CVAC) CVAC = BAC (BAC = total estimated cost)-EAC. CVAC is the the difference of total cost of the project budget and current estimates total cost of the nal completion of the project, which re ects the the deviation on the estimates cost . 5) Estimated schedule variance at completion (SVAC) SVAC (in weekly) = planning completion date-ECD. SVAC is the result of planned completion date minus the actual project completion date.

Key Benefits

Uniform measure (time or money) and therefore allows us to make simple measurements in complex situations (Ruby, 2000)

Comparability of progress in different areas of work on a consistent basis

Risk mitigation and management

Facilitates decision making and performance improvement Provides clear KPIs: - SPI (How good are doing against the plan?) - CPI (Are we efficient?)

Limitations

SPI > 1.0 does not necessarily mean you are ahead of schedule You can accomplish more work than planned by working on non-critical path work packages. You need to look at project float to determine whether you are ahead, on or behind schedule. (Lukas 2008)

References

- ↑ 1.0 1.1 Baldwin, Andrew and Bordoli, David (2014) A Handbook for Construction Planning and Scheduling, Chapter 6, p.158, First Edition, Jonn Wiley & Sons

- ↑ Lukas, Joseph (2008) Earned Value Analysis – Why it Doesn't Work, AACE INTERNATIONAL TRANSACTIONS

- ↑ Raf Dua (1999) Implementing Best Practice in Hospital Project Management Utilising EVPM methodology

- ↑ 4.0 4.1 4.2 Michael Raby, (2000),Project management via earned value, Work Study, Vol. 49 Iss 1 pp. 6 - 10

- ↑ 5.0 5.1 Kedi, Zhu and Hongping, Yang (2010), Application of Earned Value Analysis in Project Monitoring and control of CMMI, 3rd International Conference on Advanced Computer Theory and Engineering (ICACTE)