Cost build up estimation in projects

Contents |

Abstract

Cost estimation is a critical aspect of the projects management that involves predicting the likely cost of the projects and determining its feasibility based on available resources and constraints. In this wiki article, we will try to make a short mention about project cost management and cost estimation, so after we can continue and provide a holistic view of the factors that affect the costs of the projects and present the cost estimation techniques and practices that can be applied to ultimately get it as close as possible to the actual cost of each project. There is a general view that the accuracy of cost estimates is crucial to all parties involved with the projects. As a result, it is very important to analyze the factors that affect the estimation cost. There are many, but a few of the most important ones are the complexity of the project, scale and scope of the project, time, effort, market conditions, if there is an accurate plan for the project and if the tasks are clarified, experience on the methods that required to be applied, the location and accessibility of the project, the financial situation of the client. Moreover, in order to improve estimation accuracy, we must collect all the information about the factors and in conjunction with the estimation techniques, models and methodologies we will manage to make the estimation process more accurate and easier. To conclude, cost estimation is a crucial component of project management that ensures that tasks are completed on time and within budget, alternatively companies may be severely harmed from the impact of incorrect cost estimates on their finances. Project managers can make good decisions and complete their projects efficiently if they are well aware of the variables that affect cost, have a good understanding of cost estimating techniques and the importance of cost control and monitoring.

Introduction

Project cost overruns happen so regularly that, may, the operations research community should pay them greater attention, to provide further explanation of the issue of project budget overruns, to make recommendations for how to improve cost estimation as it provides a better chance for the projects to avoid hidden risks and cost blowouts. In this wiki article will strive to investigate how cost estimation can bult up in projects based on literature review in aiming to improve the performance of the project’s and to avoid wasted overruns. While many prior studies on cost estimation emphasized investigating cost estimation methods and techniques to improve the performance of cost estimation, less attention was given to the project factors that influence the cost estimating, the challenges, and the areas of implementation as well. Cost build up estimation one may say that is part of complexity perspective which, of course, is directly related to project cost management and regarding which we will make a small reference below in order to try to give a more complete and organized structure to our article. Finally, effective cost estimation is extremely important and hence project managers, it is important to have a clear understanding of the Project’s Cost, the factors that influencing cost estimations and select the appropriate methods and techniques so that the estimates are as accurate as possible. In the following sections, we will delve deeper into cost build up estimation and its significance in effective project cost management.[3],[4]

Project Cost Management Overview

Before we focus on our main topic, we will do a brief mention about project cost management, which includes the processes involved in planning, estimating, budgeting, financing, funding, managing, and controlling costs so that the project can be completed within the approved budget. The main processes of the Project Cost Management (PCM) are: Plan Cost Management − describing the process for estimating, budgeting, managing, monitoring, and controlling project costs, Estimate Costs − the process of estimating the financial resources required to finish a project, Determine Budget − a method of establishing an authorized cost baseline by combining the anticipated costs of various tasks or work packages and Control Costs − monitoring the project's progress in order to manage changes to the cost baseline and update project costs. The Project Cost Management processes are presented as discrete processes with defined interfaces, while in practice they overlap and interact in ways that cannot be completely detailed. Processes interact with each other and with processes in other Knowledge Areas.

The key concepts for project cost management, as referred to in the PMBOK GUIDE [4] are that: Project Cost Management is primarily concerned with the cost of the resources needed to complete project activities. Project Cost Management should consider the effect of project decisions on the subsequent recurring cost of using, maintaining, and supporting the product, service, or result of the project. For example, limiting the number of design reviews can reduce the cost of the project but could increase the resulting product’s operating costs. Another aspect of cost management is recognizing that different stakeholders measure project costs in different ways and at different times. For example, the cost of an acquired item may be measured when the acquisition decision is made or committed, the order is placed, the item is delivered, or the actual cost is incurred or recorded for project accounting purposes. In many organizations, predicting and analyzing the prospective financial performance of the project’s product is performed outside of the project. In others, such as a capital facilities project, Project Cost Management can include this work. When such predictions and analyses are included, Project Cost Management may address additional processes and numerous general financial management techniques such as return on investment, discounted cash flow, and investment payback analysis.

Cost estimation Overview

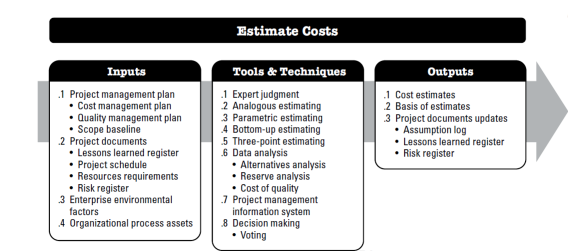

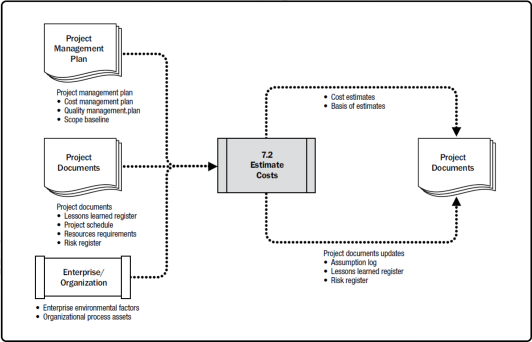

Cost estimating involves developing an approximation (estimate) of the costs of the resources needed to complete project activities. It is a prediction that is based on the information known at a given point in time. Cost estimates include the dentification and consideration of costing alternatives to initiate and complete the project. Cost trade-offs and risks should be considered, such as make versus buy, buy versus lease, and the sharing of resources in order to achieve optimal costs for the project. The key benefit of this process is that it determines the monetary resources required for the project. This process is performed periodically throughout the project as needed. Cost estimates are typically represented in units of some currency (e.g., dollars, euros, yen, etc.), but in some cases, other units of measure are used to assist comparisons by removing the impacts of currency fluctuations, such as staff hours or staff days. Cost estimates should be evaluated and adjusted during the project to take into account new information as it becomes available and hypotheses are tested. As a project moves through the project life cycle, its estimation accuracy will rise. A project at the start phase, for instance, might have a rough order of magnitude (ROM) estimate that falls between 25% and +75%. As the project progresses and more information becomes available, precise predictions may reduce the range of accuracy to 5% to 10%. There are rules for when such improvements can be made and the level of confidence or accuracy that is expected in specific businesses. Costs are estimated for all resources that will be charged to the project. This includes, but is not limited to, personnel, supplies, tools, services, and facilities, as well as unique categories such as inflation allowance, financing charges, or unforeseen expenses. Cost estimates can be displayed in summary or at the activity level. The inputs, tools and techniques, and outputs of this process are depicted in Figure1. Figure 2 depicts the data flow diagram of the process.

Figure 1. Estimate Costs: Inputs, Tools & Techniques, and Outputs

Figure 1. Estimate Costs: Inputs, Tools & Techniques, and Outputs

Figure 2. Estimate Costs: Data Flow Diagram

Figure 2. Estimate Costs: Data Flow Diagram

Factors influencing cost build up estimating

When creating the cost estimate, the estimating department takes a broad view of the project and considers several variables, including expected output levels during the construction stage. The estimating department determines the consolidated cost estimate by considering the resources needed for the project in terms of quantity, quality, cost, and performance, as well as other factors (such as the extent of information requirements, project environment, etc.) that may affect the performance of those resources. [1]

In a more general perspective factors that influencing cost build up estimating can be divided into four main categories:

- Project-specific factors

- Resource factors

- Environmental factors

- Economic factors

Since the construction industry has influenced most of the literature that has been written regarding cost build up estimation projects, the following factors are the most crusial:

- Complexity of design and construction

- Method of construction/construction techniques

- Tender period and market condition

- Site constraint - access and storage limitation

- Clients’ financial situation and budget

- Location of project

- Availability and supplies of labor and materials

- Project team’ s experience of the construction type

- Lead times for delivery of materials

- Form of procurement and contractual arrangement

- Amount of special work / likely production time

- Off/on-site operations sequencing and limitations

- Expertise of consultants

- Number of project team members [1]

It's important to consider all these factors when estimating project costs, to ensure that the estimate is accurate and reflects the actual cost of completing the project. Project managers must use their judgment and expertise to make informed decisions about these factors when estimating costs.

Cost estimation techniques

Product cost estimation techniques:

Qualitative techniques

- Intuitive-estimates are based on the expert estimator’s experience.

- Analogical-estimates made on the definition and the analysis of the degree of similarity between the new product and another one for which cost has been estimated in the past.

Quantitative techniques

- Parametric-estimates based on an analytical function of a set of parameters characterising the product, without describing it completely. These are known to be top-down applications.

- Analytical-based on a detailed analysis of the work required into the elementary tasks that constitute the manufacturing process. This is also termed as bottom up techniques where the cost data are collected from the smallest component levels and aggregated to the total product level.

Service cost estimation techniques:

• Expert opinion or judgment. Expertise should be considered from individuals or groups with specialized knowledge or training in the following topics:

• Previous similar projects.

• Information in the industry, discipline, and application area; and

• Cost estimating methods.

• Top-down costing. Top-down costing first calculates the total costs of the service at the organisational, provider or departmental level, then disaggregates the total costs to the department or the units of services (or products) depending on the richness of available data and the homogeneity of services provided. It can be done through multiple steps, e.g., allocate costs to cost centres (e.g., support services workshop, project management), then divide the total costs of the cost centre by the number of units (e.g., spares supplied, etc.) Top-down approach is less detailed and so accuracy can suffer. Furthermore, allocation of resources can be more or less arbitrary.

• Bottom-up estimating. Bottom-up estimating is a method of estimating a component of work. The cost of individual work packages or activities is estimated to the greatest level of specified detail. The detailed cost is then summarized or “rolled up” to higher levels for subsequent reporting and tracking purposes. The cost and accuracy of bottom-up cost estimating are typically influenced by the size or other attributes of the individual activity or work package.

• Parametric estimating. Parametric estimating uses a statistical relationship between relevant historical data and other variables (e.g., square footage in construction) to calculate a cost estimate for project work. This technique can produce higher levels of accuracy depending on the sophistication and underlying data built into the model. Parametric cost estimates can be applied to a total project or to segments of a project, in conjunction with other estimating methods.

• Analogous estimating. Analogous cost estimating uses values, or attributes, of a previous project that are similar to the current project. Values and attributes of the projects may include but are not limited to: scope, cost, budget, duration, and measures of scale (e.g., size, weight). Comparison of these project values, or attributes, becomes the basis for estimating the same parameter or measurement for the current project.

• Three point estimating. The accuracy of single-point cost estimates may be improved by considering estimation uncertainty and risk and using three estimates to define an approximate range for an activity’s cost:

• Most likely (cM). The cost of the activity, based on realistic effort assessment for the required work and any predicted expenses.

• Optimistic (cO). The cost based on analysis of the best-case scenario for the activity.

• Pessimistic (cP). The cost based on analysis of the worst-case scenario for the activity.

Depending on the assumed distribution of values within the range of the three estimates, the expected cost, cE, can be calculated using a formula. Two commonly used formulas are triangular and beta distributions. The formulas are:

• Triangular distribution. cE = (cO + cM + cP) / 3

• Beta distribution. cE = (cO + 4cM + cP) / 6

Cost estimates based on three points with an assumed distribution provide an expected cost and clarify the range of uncertainty around the expected cost.

• Data analysis.

Data analysis techniques that can be used in the Estimate Costs process include but are not limited to:

• Alternatives analysis. Alternatives analysis is a technique used to evaluate identified options in order to select which options or approaches to use to execute and perform the work of the project. An example would be evaluating the cost, schedule, resource, and quality impacts of buying versus making a deliverable.

• Reserve analysis. Cost estimates may include contingency reserves (sometimes called contingency allowances) to account for cost uncertainty. Contingency reserves are the budget within the cost baseline that is allocated for identified risks. Contingency reserves are often viewed as the part of the budget intended to address the known-unknowns that can affect a project. For example, rework for some project deliverables could be anticipated, while the amount of this rework is unknown. Contingency reserves may be estimated to account for this unknown amount of rework. Contingency reserves can be provided at any level from the specific activity to the entire project. The contingency reserve may be a percentage of the estimated cost, a fixed number, or may be developed by using quantitative analysis methods.

As more precise information about the project becomes available, the contingency reserve may be used, reduced, or eliminated. Contingency should be clearly identified in cost documentation. Contingency reserves are part of the cost baseline and the overall funding requirements for the project.

• Cost of quality. Assumptions about costs of quality (Section 8.1.2.3) may be used to prepare the estimates. This includes evaluating the cost impact of additional investment in conformance versus the cost of nonconformance. It can also include looking at short-term cost reductions versus the implication of more frequent problems later on in the product life cycle.

• Mixed approach

[2],[4]

Challenges and areas of implement

There are many things that could be done better. The risks that have been identified in all the aforementioned examples are primarily equipment-related risks, with minimal consideration for consumer value. Understanding the relationship between client satisfaction and expenses is crucial for tracing the origins of profitability at the customer level as the need for businesses to become more customer-centric grows. There are no studies specifically focusing on the dangers associated with this link between cost and value. There is still room for more study in this area. The cost modeling of availability-type contracts still has room for improvement in terms of accuracy and joint cost modeling.

Conclusion

References

[1] Analysis of factors influencing project cost estimating practice, AKINTOLA AKINTOYE Department of Building and Surveying, Glasgow Caledonian University, Cowcaddens Road, Glasgow G4 0BA, UKReceived 10 June 1998; accepted 17 December 1998 [2] Cost modelling techniques for availability type service support contracts: A literature review and empirical study. Partha P. Datta a,*, Rajkumar Roy b [3] The moderating effect of project complexity on the relationship between organizational controls and cost estimation performance: A conceptual model. M W Fazil, C K Lee and P F M Tamyez, 2022 [4] A Guide to the PROJECT MANAGEMENT BODY OF KNOWLEDGE, (PMBOK® GUIDE) Sixth Edition,2017